Following the Government’s budget announcements in late-2024 and concerns over the impact of the new administration in the United States, retailers entered 2025 cautiously.

New measures to protect UK High Street from aggressive rent collection and closure

Tech savvy manufacturers set for £13bn boost as they cut out wholesalers and shops to sell direct to consumers

Independent retail hit by a loss of -1,554 units in first six months of 2018

Independent retail hit by a loss of -1,554 units in first six months of 2018.

Data released today by the British Independent Retailers Association (bira) and the Local Data Company (LDC) shows that independent retailers opened significantly more shops in H1 2018 than in the same period last year. However, a record number of stores were closed over the same period. This resulted in a total decline of -1,554 independent shops (-0.5%) - a significant decline from the increase of +762 shops (+0.27%) seen in H1 2017. The net loss of -695 units located on high streets alone was the main driver of this decline. Independent units categorised as ‘Service Retail' (including retailers such as barbers, hairdressers and dry cleaners) was the only category to see growth, with a net increase of +104 units in H1 2018.

Chain retailers (brands with more than 4 stores) have also remained in decline with a net loss of -2,848 shops (-1.36%) in H1 2018 across GB, which compares to -659 shops (-0.33%) in H1 2017.

Key information

Independents account for 65% of all retail and leisure units in Great Britain, the same as H1 2017.

In H1 2018 a total of 32,234 independents either opened (15,340) or closed (16,894), 14.8% up on H1 2017 where 28,076 opened (14,419) or closed (13,657).

The comparison goods retail category (non-perishable goods such as clothes, books and homewares) saw a net change of -1.63% in H1 2018 (-0.74% in H1 2017). This is a net decrease of -1,394 units, significantly higher than the -596 net change recorded in H1 2017.

Numbers of independent leisure units (including restaurants, cafes, bookmakers & entertainment) stayed the same in H1 2018 with no net change (0.00%) compared to a +0.55% increase in H1 2017. In H1 2018 there was a no change in the number of units (4,761 openings and 4,761 closures), versus a net increase in units of +475 net change in H1 2017.

The convenience retail category (bakers, butchers, food shops, & supermarkets) saw a net decline of -264 units (-0.86%) in H1 2018 versus a small increase of +24 units (+0.08%) in H1 2017.

Service retail (health & beauty, financial services, tattoo parlours and estate agents) was the only category of independents to see an increase in H1 2018 of +104 units (+0.10% versus +0.94% in H1 2017).

Key growth sectors have been barbers, beauty salons, tobacconists/e-cigarette shops, and Mobile phones. (see table 1 for more detail)

Sectors in decline include estate agents, newsagents, women’s clothing shops, and fashion shops. (see table 2 for more detail)

Vegan restaurants (+32%) and Vaping/Tobacconists (+6.7%) have increased the most as a percentage of their total units

The West Midlands showed the greatest increase of independents at +117 units (+0.49%) in H1 2018, versus +194 units (+0.93%) in H1 2017

Yorkshire & the Humber and Greater London saw the greatest decline of independents at -494 units (-1.64%) and -276 units (-0.40%) respectively

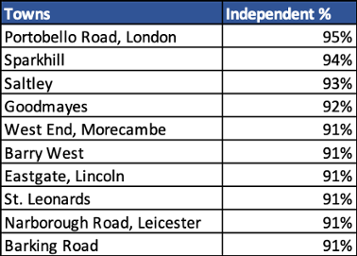

Portobello Road in London has the accolade of having the highest percentage of independents at 95% (based on locations with 50+ total units) overtaking Sparkhill in Birmingham (2nd) which was the top location in H1 2017

Ellenbrook is the town with the lowest percentage of independents at only 19%, against a GB average of 65% (based on locations with 50+ units)

Wider analysis of location types (analysis of location types by high streets, shopping centres and retail parks) shows that high streets saw a dramatic decline of -695 units in H1 2018. This represented a -0.41% net decrease in units.

Shopping centres saw a similar pattern in H1 2018 with a decline of -1.55% (versus +0.67% in H1 2017). Retail parks was the only location type to see growth in units of +1.48% (versus +3.41% in H1 2017) however this location type only accounts for 0.2% of all independents across GB.

Top 10 independent business openings by retail category

Table 1. Highest numbers of independent units opened by business type in H1 2018 across GB (Source: LDC)

Top 10 independent business closures by retail category

Table 2. Highest numbers of independent units closed by business type in H1 2018 across GB (Source: LDC)

National and regional net variations of independents

Table 3. Net percentage change (openings minus closures) of independent units by region in H1 2018 across GB (Source: LDC)

Top 10 independent towns (50+ units)

Table 4. Towns with the greatest percentage of independent retailers (Source: LDC)

Bottom 10 independent towns (+50 units)

Table 5. Towns with the lowest percentage of independent retailers (Source: LDC)

Change in numbers of independents by location type

Table 6. Net change by location type for Independents across 2,700 in and out of town GB locations (Source: LDC)

Further comment from Lucy Stainton:

Lucy Stainton, Senior Relationship Manager, Local Data Company commented:

“There is no doubt 2018 has already shown itself to be a particularly transformative year for the UK retail market. The shake-up across the physical landscape is impacting chains and independents alike. Businesses in all corners of the industry are having to look very closely at their current model and assess its relevance in an era of unprecedented consumer change. It is not all bad news for independent businesses though, if we look to the leisure sector, which has fallen into sharp decline for the first time in the first half of 2018, this has been driven entirely by a fall in chain outlets. Independents on the other hand have been able to take advantage of the consumer’s increased search for uniqueness.”

Andrew Goodacre, CEO, British Independent Retailers Association (bira), said

“This report perfectly illustrates the problems for independent retail businesses. Despite more businesses opening, we have seen more closing resulting in a net loss from the high street. bira have been saying for a long time that independent retailers need support from local and national governments. The recent budget announcements regarding a rates reduction and the setting up of a high street fund are very welcome and we hope it is not too late to provide a lifeline to these important businesses.”

Note: The total number of independent businesses covered in this research across GB was 310,080

UK FOOD RETAILERS FACE £9.3BN NO-DEAL BREXIT BILL

· Failing to reach a Brexit deal could cost food retailers and their supply chain £9.3 billion, according to a new Barclays Corporate Banking report

· A no-deal, Brexit model would create an average tariff of 27% for food and drink supply chains

· With grocery margins typically around 3–5%, additional cost is likely to end up being passed on to consumers

As Brexit negotiations continue, a new report shows retailers could face additional tariffs totalling £9.3bn per year for food and drink products imported from the EU if a settlement isn’t reached. The new Barclays report, Scale, Disruption and Brexit – a new dawn for UK food supply chains? shows that in a no-deal Brexit, food retailers would be affected by a new average tariff of 27% on food and drink goods entering from the EU, significantly more than the 3-4% levy that would hit non-food products. Additionally, every consignment of goods from the EU will require a customs declaration which starts at a minimum of £50.

Last year, the UK imported £48bn worth of food and drink, approximately 40% of the total UK market. Of these, 71% originating from within the EU entered the UK free of customs duties and other trade costs. While a free trade deal or the Chequers option, would help the food industry avoid tariffs and related duties, a no-deal Brexit could mean significantly higher costs for retailers and consumers.

Ian Gilmartin, Head of Retail at Barclays Corporate Banking, comments: “The food and drink industry is one of the country’s most important sectors, employing millions of people across the UK. For the good of both UK business and consumers, the potential impact on our producers and grocery retailers should be front and centre of Brexit negotiations.

“Some products would avoid tariffs, even in a no-deal scenario, but for most goods the effect of an increased tariff burden would be extremely damaging, and cheaper goods would be the hardest hit. 71% of our imported food and drink comes from the EU, and 60% of our exports go to the EU. A positive agreement on trade is essential if we are to protect UK exporters and avoid significant price rises for UK consumers.”

The cost of a no-deal Brexit

Food retailers are waiting to see whether a ‘Brexit deal’ can be reached that keeps costs down for the sector. A full customs union, for example, would maintain the current tariff-free trade enjoyed by the UK and the EU but would limit the UK’s ability to trade unilaterally with other countries. A free trade agreement (FTA) would be likely to minimise the amount and cost of new tariffs imposed on trade. Though an FTA would still require extra fees from logistics, such as customs declarations, it would also free the UK to make other trade deals.

However, a no-deal Brexit would impose significant costs on food retailers, with varying tariffs for different types of products. For example, the Barclays report shows that fully processed food and drink products, such as orange juice, will attract the highest tariff rate of 31% compared to 29.5% for semi-processed food and drink such as white sugar, and 9.7% for primary products and raw materials like bananas.

Beyond such category based surcharges, some products also attract ‘specific duties’, which are tariffs levied on a per unit basis; that is, by weight or volume. The Barclays report shows specific duties disproportionately target certain products including meat, cereal, olive oil, wine and sugar-based foods. By their nature, these tariffs place a higher burden on lower-value transactions.

Hardest hit will be those products that attract both a category tariff as well as a specific duty tariff, such as frozen beef with a specific duty of 298%. Common cooking products also face steep duties including beef cuts at 101%, cream at 81% and garlic at 71%.

Further costs could also mount under a hard Brexit. In addition to customs declarations, comes the burden of complying with stringent EU Sanitary and Phytosanitary (SPS) regulations, which could be the equivalent of paying an extra 8% in duty tax on EU food and drink imports.

Backdrop to Brexit

While Brexit is currently the most pressing issue for food retailers, wider consumer trends are also providing new challenges and opportunities. As the pace of life becomes busier, shoppers are visiting stores more often, with trips up 14.3% from 2013 to 2018, but buying less per visit, with average spend down 8.5% during the same period². According to the Barclays report, the convenience sector has been growing at an above-average rate, at 10% over the past four years compared to 7.1% for the industry – and is now worth £40bn³. Likewise, the online food market has grown by an average of 12% since 2010⁴.

At the same time, as wider economic upheaval has pinched household budgets, consumers have turned to discount food retail outlets such as Aldi and Lidl, leading to the ‘Big Four’ facing a nearly 10% decline in market share since 2011. With many food retailers already struggling to adapt to a changing British market, Brexit negotiations could be adding an extra layer of uncertainty.